Future USS: Robin Hood can help?

In this post I’ll follow up on the previous one, USS pension scheme and fairness, in the light of this week’s UCU proposals (proposals which provide a basis for renewed talks with Universities UK about the future of USS).

My purpose here is to suggest that a fairer solution could also be more affordable — in that it would help fund the defined-benefit section of USS, but would also reduce (and might perhaps even eliminate?) the upward pressure on employer and employee contribution rates.

1. The current UCU proposals

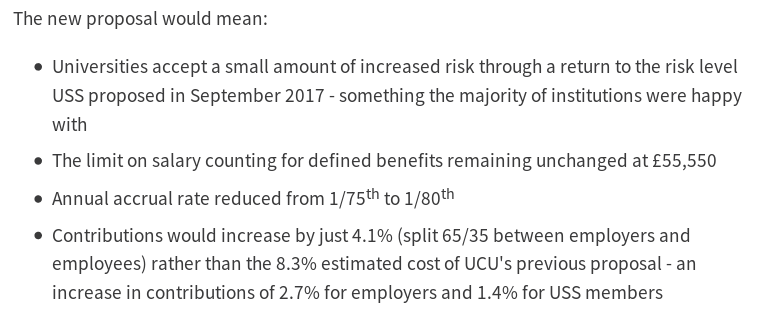

The following summary excerpt is taken from https://www.ucu.org.uk/article/9364/Further-talks-agreed-in-universities-pensions-dispute:

The University and College Union (UCU) deserves all of the many congratulations it is currently getting, for having produced such a proposal this week — in particular, a proposal that has at last persuaded the employers (Universities UK) to take part in further talks about the future of USS.

That said: I should admit to feeling disappointed by the 3rd and 4th bullet points above! USS members would all be getting a slightly worse pension, in return for an appreciable increase in the contribution rates (both employee and employer contribution rates).

More crucially — if I have understood it correctly — the implied loss of pension (as a percentage of contributions paid) would be greatest for those USS members whose salary is £55k or lower. Higher-paid members of USS would be required to make a smaller sacrifice — substantially smaller, in the case of those with the very highest salaries — relative to the overall size of their pensions.

Recognising this unfair distribution of the pain, and thinking about how best to fix it, leads naturally to an additional device that could make the proposed changes fairer and more easily affordable.

2. Robin Hood to the rescue

The current USS setup has a slightly progressive aspect, which is that the 18% employer contribution for salary over the £55k threshold pays only 12% into the member’s defined-contribution (DC) pension pot. The remaining 6% therefore helps to support the running costs of USS, and (mainly, it seems safe to presume) the defined-benefit part of USS.

The suggestion I want to make here is that future USS should become more progressive — that is, USS should move further in that same, progressive direction. (As mentioned in the previous post, the current USS proposal would increase that 12% figure to 13.25%, thereby making the scheme appreciably less progressive. And as I have argued in that previous post, that seems completely indefensible.)

The specific suggestion:

-

For salary between the current £55k threshold and some specified higher threshold, pay x% from the employer contribution into the employee’s DC pot. The value of x could be left at 12, for example.

-

For salary above the higher of the two thresholds, pay y% from the employer contribution into the employee’s DC pot, where y is smaller than x.

Even if x remains at 12, such a device would allow (through suitable choice of the higher threshold and the value of _y) _substantial savings to be made from the employer contributions on higher salaries — savings which could then be used directly to support the threatened, defined-benefit part of USS.

The precise arithmetic on this becomes possible only with detailed knowledge (not available to me) of the distribution of USS-member salaries over £55k. Some general considerations on the choice of the higher threshold, and of y, are:

- The higher threshold clearly should not be so high as to make the resultant savings too small to be of much consequence.

- The value of _y _probably needs to be at least as high as the employee contribution rate (currently 8%), otherwise it could become unattractive for those with the highest salaries to remain in USS.

Illustrative example:

Just to give a sense of what might be possible through this device. Let’s suppose:

- salary between £55k and £75k gets 12% into the DC pot, from the employer contribution — as now.

- salary over £75 gets 8% (i.e., the current employee contribution rate) instead of 12%.

Then the amount saved, which could then be used to support the defined-benefit part of USS, would be 4% of all member salaries over £75k.

3. Conclusion

It is unclear to me, in absence of enough data to determine it, whether the ‘Robin Hood’ device just described would be enough to completely eliminate the need for a change in the accrual rate and/or increased contributions (as proposed by UCU in their points 3 and 4 above).

What is clear to me, though, is that such a device would help eliminate the unfairness described above. And it would, at least, reduce the need for any changes in accrual or contribution rates, even if such need is not completely eliminated.

Update on 16 March: After reading this post, you might perhaps be interested in some of these follow-ups:

- Latest USS proposal: Who would lose most?

- USS proposals: Tail wagging the dog?

- Simple maths of a fairer USS deal

© David Firth, March 2018

To cite this entry: Firth, D (2018). Future USS: Robin Hood can help? Weblog entry at URL https://DavidFirth.github.io/blog/2018/03/01/future-uss-robin-hood-can-help/

Postscript: about Robin Hood

The legend of Robin Hood, ‘feared by the bad, loved by the good’, will already be known to most people who have grown up in England. There are countless stories of Robin Hood ‘persuading’ the rich to part with their money, for the benefit of poorer folk.

For anyone interested, there’s a lot to read about it here: http://www.robinhoodlegend.com/.

One aspect that I particularly like is that my home city of Wakefield is one of the (many!) places that lay claim to Robin Hood as one if its own townspeople. But then there’s all that romantic Sherwood Forest nonsense…